profile/9484image0.png.webp

Mark_

An Overview Of Custom Truck One Source, Inc.s Income Statement, 2024

~1.7 mins read

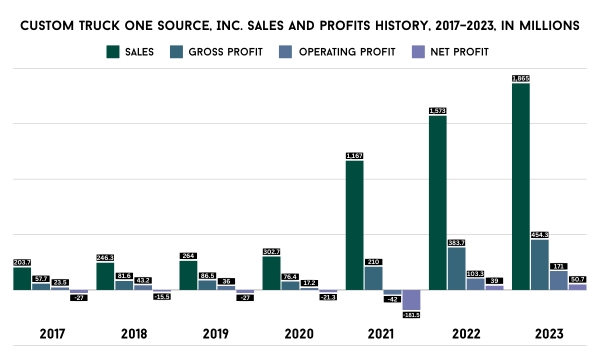

Custom Truck One Source, Inc.’s sales for the past 7 years show a consistent upward trend, just like gross profit. However, as you can see, operating profit is inconsistent, and net profit has only recently started to be positive and increase bit by bit.

This is due to increasing expenses, particularly COGS and operating costs, which have been on an upward trend for a long time and are significantly reducing profits. Compared to 2017, in 2023, both COGS and operating expenses grew by approximately 9 times.

Selling, general, and administrative expenses account for a large portion of operating costs, and as a percentage of gross profit, they far exceed the 30% threshold, which investors think is appropriate.

Though Custom Truck One Source, Inc.’s EPS was negative due to losses, it was also showing an upward trend, resulting in losses getting smaller each year until EPS finally became positive in 2022 and 2023. Finviz.com estimates that the next year’s EPS will be 0.27 USD, slightly higher than it was in 2023.

Most of the time, its gross margin exceeds 20%, but it falls significantly short of the generally accepted 40% threshold. Additionally, the operating and net margins are too low and inconsistent. At least in 2022–2023, all the profit margins became positive and are increasing, which means that the company finally became profitable and somewhat stable.

The company’s depreciation is increasing most of the time, and as a percentage of gross profit, it is far higher than the desired 6–8%. However, at least the percentage is decreasing over time, so it might reach the desired value in the near future.

Custom Truck One Source, Inc.’s operating ratio has mostly remained the same, with a slight decrease in recent years, which is what investors look for. Interest expenses, on the other hand, are increasing in the same way as COGS and operating expenses, but as a percentage of operating income, they far exceed the desired 6–7% value investors look for.

In conclusion, the data from Custom Truck One Source, Inc.’s income statements and related KPIs did not reveal any competitive advantages, since most of the KPIs performed poorly or averagely, but to make sure that there are none, it is necessary to check its other financial statements too.

profile/9484image0.png.webp

Mark_

Alta Equipment Group Inc.s Cash Flow Statements, 2019-2023

~1.5 mins read

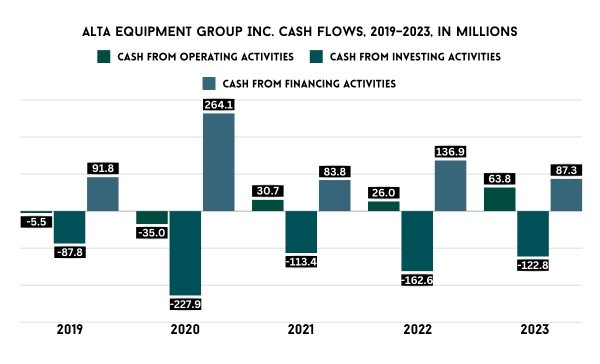

In this article, we’ll take a closer look at Alta Equipment Group Inc.’s KPIs from the cash flow statement, and the first one will be its cash flows for the past five years:

The company’s cash from operating activities is showing an upward trend, while investing activities do not provide the cash at all due to huge expenditures on property, equipment, and acquisitions.

Cash from financing activities, on the other hand, is always positive because the company borrows money. The company uses credit lines, long-term borrowings, and floor plan financing.

Both capital expenditures and dividends at Alta Equipment Group Inc. are increasing. While it’s good when dividends are growing, capital expenditures should decline, or at least stay at the same level.

Stock repurchases and issuances rarely occur, as you can see on the chart. Despite the lack of benefits for shareholders from stock buybacks, this situation ultimately benefits the company and its shareholders in the long run, as the company actively engages in growth and expansion, making use of available resources.

Alta Equipment Group Inc.’s free cash flow is constantly negative due to CAPEX being higher than cash from operating activities, but its overall trend is also heading in the right direction, as you can see in the picture.

Its CAPEX to net income ratio is too high; it far exceeds 25%, which is considered desirable by investors, but again, the company spends a lot of resources on growth and expansion, so in the future this ratio might stabilize.

In conclusion, Alta Equipment Group Inc.’s cash flow statement showed that the company is getting better year over year in some aspects, such as dividends, cash from operating activities, etc., but it also revealed that the company relies heavily on debt to sustain itself.

Advertisement

Link socials

Matches

Loading...